CLOSE SIDEBAR

CLOSE SIDEBAR

Event Study: Measuring Investor Enthusiasm in the Stock Market; Do investors pay more attention to the information technology sector?

Jake Woolard and William Pesto

William Pesto and Jacob Woolard

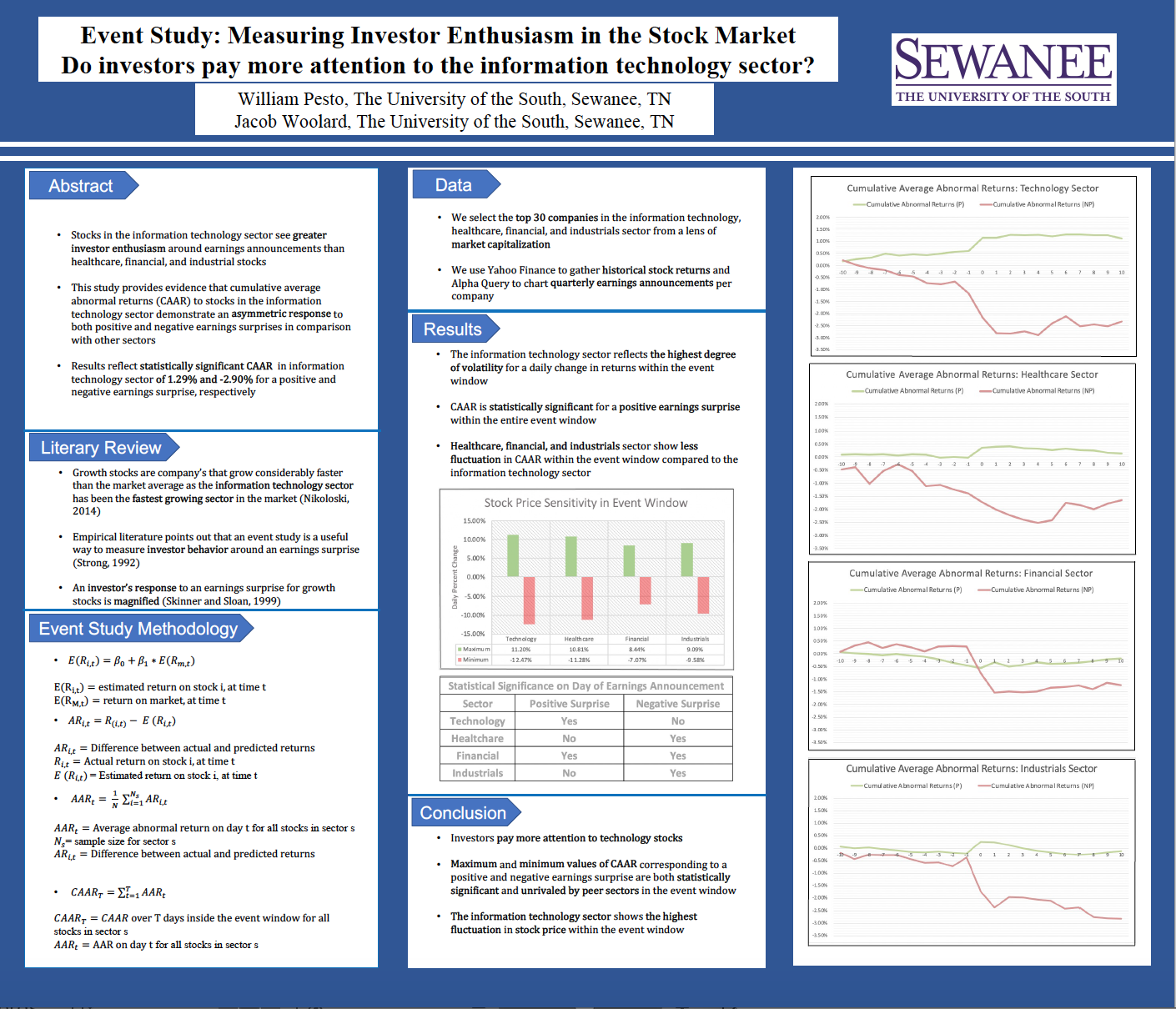

We provide evidence that cumulative average abnormal returns (CAAR) to stocks in the information technology sector are linked to investor enthusiasm arising from a positive earnings surprise while a negative earnings surprise coincides with less returns than companies in the healthcare, financial, and industrials sectors. The attractive growth profile of stocks in the information technology sector results in investors demonstrating an asymmetric response to both positive and negative earnings surprises yielding statistically significant CAAR of 1.29% and -2.90%, respectively. Through assessing stock price sensitivity in the event window, the information technology sector reflects the highest degree of sensitivity across comparable sectors for a daily increase and daily decrease in value. While investors show greater enthusiasm towards growth stocks in this sector with a positive earnings surprise, they are cautious of growth stocks releasing a negative earnings surprise due to the elevated risk associated with holding the stock.

Powered by Acadiate

© 2011-2024, Acadiate Inc. or its affiliates · Privacy